As the CMA investigation into the acquisition of Substantial Group (better known as Netomnia) by nexfibre plods along, nexfibre commissioned a report by Assembly Research into looks into the implications of the merger and highlights potential dangers if the investigation drags on for many months.

We’ve previously reported on the impact of the acquisition in terms of footprints back in February 2026, and this is referred to in the report. With full fibre roll-outs continuing exact figures will have changed, so for example our nexfibre XGS-PON footprint has risen from 2.12 million to 2.62 million premises Ready for Service and the Substantial Groups footprint is up from 3.07 million to 3.12 million premises.

A more significant change is that giffgaff who are owned by Virgin Media O2 is growing its use of the nexfibre XGS-PON network and is offering full fibre services in selected FibreUp/Project Mustang areas via the nexfibre wholesale platform. giffgaff while part of the VMO2 stable is offering things like no mid term price rises and 24 or 1 month contracts so looks very like what you’d expect a wholesale customer to offer.

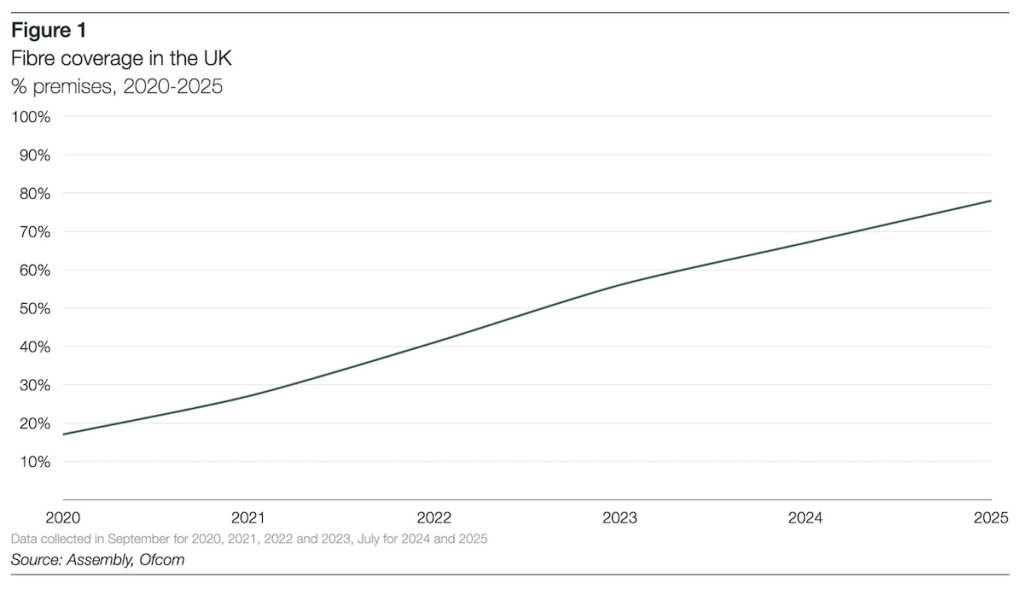

Back to the report and a cautionary note we’d urge the wide range of people interested in this acquisition is fully aware of and that is the full fibre market of Sept 2020 to July 2025 is now very different eleven months later.

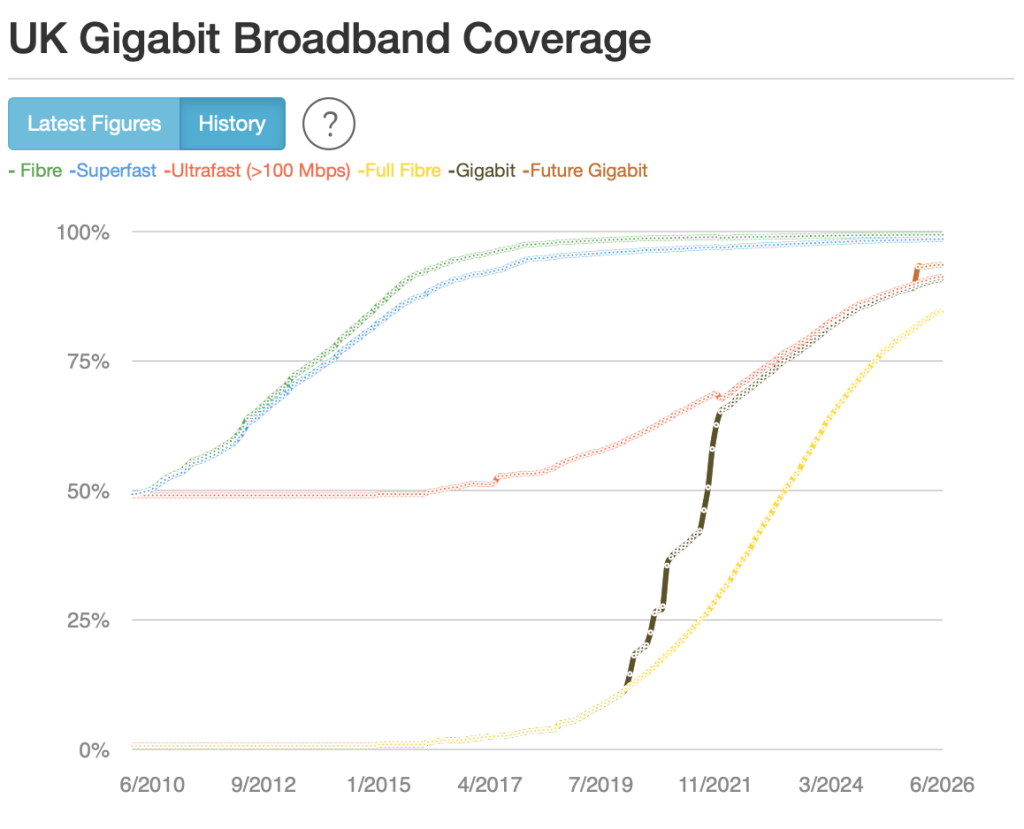

The chart produced from the Ofcom Connected Nations data suggests a near linear growth in full fibre footprint, but since the summer of 2025 the slow down as the withdrawal of easy access to funding for full fibre builds really too effect is visible in our much more frequently updated data.

Back at the start of July 2025 our figure for the UK was 78.3% full fibre coverage lining up with Ofcom data, by the end of July 2025 it had reached 79.1%. In the subsequent 11 months footprints have risen to 84.5% of UK premises and while still rising a classic S-curve is now visible showing how rollouts are slowing, and overbuild is becoming more common.

Understanding this is important to any CMA decision making since in that we have left the golden age of full fibre investment and are now in a consolidation phase that will then define the market for 2030 and onwards.

A danger highlighted in the report is that if the CMA decision and approval for the deal stretches well into 2027 then the alt-net market will suffer. While the £3.5 billion nexfibre/Substantial transaction just involves those two companies it is seen as a litmus test for the market and will set a pattern going forward, and with the financial situation continued uncertainty could see some alt-nets suffer and potentially collapse. Broadband firms getting into financial trouble is not new, but with no formalised Provider of Last Resort mechanism in the UK things could get complicated and messy for the public very quickly.

At the time the nexfibre/Substantial transaction was announced, the impact of nexfibre using the Substantial build model and resources to expand XGS-PON footprints was a bit lost in the excitement and comparisons between a possible CityFibre/Substantial transaction. The Assembly Research report and what has been said since the transaction become public knowledge highlights that this does appear to be about creating a nexfibre wholesale platform that will have sufficient size to take on Openreach wholesale.

nexfibre being a scaled challenger to Openreach who are aiming to have a network ready to service 30 million premises by 2030 is very important. Why? Because if altnets and nexfibre are all in the 50,000 to 8 million footprint region Openreach will be the dominant player and we’ll have gone from them being the dominant copper player to the dominant full fibre one. If nexfibre can scale to a footprint of 19 million or even better 22 or 23 million for 2030 the UK broadband landscape will be much healthier in terms of competition. While this looks like a duo-opoly if the alt-net market can challenge those two in around 40% of the UK market things will be much healthier than the 2000’s and 2010’s.

Why does competition matter? I made a small warning on price rises and other effects of the latest Openreach price offers on Monday prior to visibility of the Assembly Research report they are more coherent in their summary and warn that average pricing we see today is not likely to be sustainable.

“Competing on prices that are considered too low has challenged the financial prosperity of the altnet market, with suggestions that some may need to raise retail average revenues per user (ARPUs) significantly just to break even. Most altnets reportedly have ARPUs of between £25 and £35, which may need to rise to £40 or higher to place them on a sustainable financial footing that allows for future investment. CityFibre recently explained that its full fibre wholesale pricing is up to 37% cheaper than Openreach’s. While this may make CityFibre a commercially attractive option for wholesale customers, such competitive pricing may not be possible for many altnets to offer or sustain.”

Assembly Research on ARPU (average revenue per unit)

There is no model that says how many networks are needed for full fibre to remain competitive for price and service but the 2009 time when it was Openreach versus Virgin Media in just around 40-45% of the UK is not that model.

To paraphrase some comments made by Rajiv Datta the CEO of nexfibre at a meeting discussing the report, the investment market has left the full fibre game and is very focused on AI for now, and that has big implications for how mergers and acquisitions will happen going forward. The difficulty in getting investment for full fibre now is real.

The key now is nexfibre continuing to build both in new areas and attracting a retailer onto its wholesale platform. Also Government and Ofcom doing all that is can to support the sector and encourage investment so that firms can afford to both build more full fibre and connection paying customers. Connecting paying customers is the focus among alt-nets today, but the cost of the work to visit and install each home can take years to recover, the short term advantage is showing better take-up figures so that investors don’t run off to a better investment vehicle.

The full 28 page report is available as a PDF so you can read the Assembly Research conclusions and analysis directly.

“Assembly’s report captures the reality of the UK fibre market today and reinforces that the next phase must be about scale, sustainability and genuine long-term competition.

That’s why our planned acquisition of Netomnia is a real turning point for the industry; creating a wholesale challenger with the footprint and funding needed to compete properly at a national scale.

By bringing together complementary assets and unlocking further investment, the transaction can help support the market structure the UK needs: one that protects infrastructure competition, gives ISPs more choice, and delivers better outcomes for consumers and businesses.“

Rajiv Datta, CEO, nexfibre

“The proposed acquisition of Netomnia by nexfibre is an example of the next chapter in the UK’s fibre story where the market needs to move from fragmentation to consolidation. Bringing together scale and capital will be the key ingredients to create a stronger rival to Openreach in line with the policy goal of enduring infrastructure-based competition.“

Matthew Howett, Founder, Assembly Research

In terms of a challenger to Openreach if the transaction gets approval by the end of 2027 with the nexfibre footprint, Netomnia footprint and 2.1 million old coax addresses given access to XGS-PON via expansion nexfibre is looking at a footprint around 8 million full fibre premises.

One further comment to add from the report and meeting is that if Openreach is interested in de-regulation across substantial parts of the UK having a real wholesale competition on both price and product performance is a key requirement.

Test your broadband speed

Test your broadband speed Follow us on X for the latest broadband news

Follow us on X for the latest broadband news

Leave a reply