The acquisition of Netomnia (Substantial Group) and the retail customers of YouFibre and brsk is set to be a big change in the Altnet market, so what is Virgin Media O2 (VMO2) going to gain?

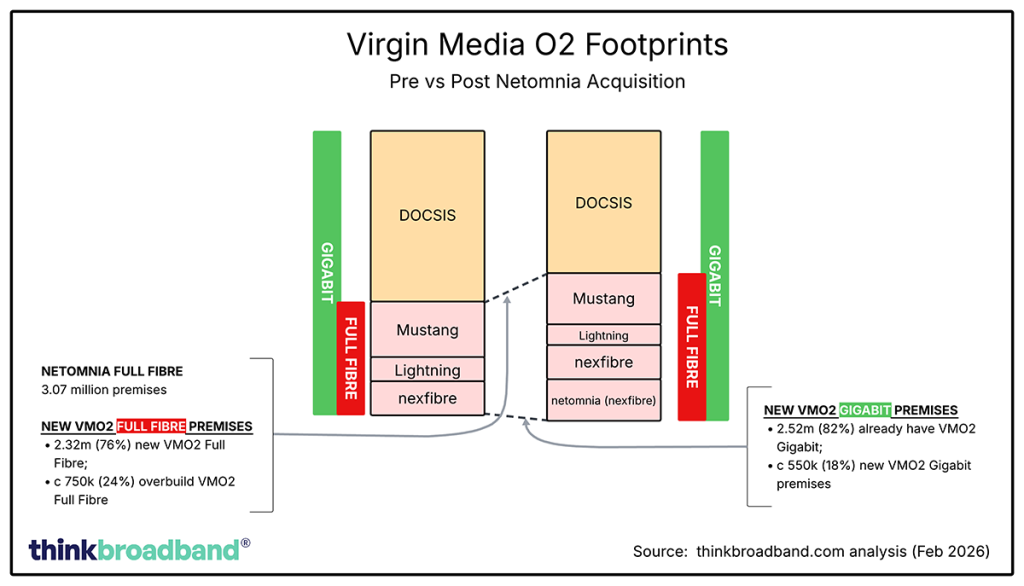

The £2 billion purchase brings them the Netomnia full fibre footprint, which we have mapped at 3.07 million premises. It is being acquired by the shareholders of VMO2 and Nexfibre, with the retail services being resold to VMO2 and the infrastructure remaining with Nexfibre. (The number we have verified may slightly lag behind the numbers used in the transaction).

Of these 3.07m premises, the overlap breakdown with the different Virgin Media O2 footprints is as follows: –

- 0.38 million (12%) are in areas where Project Mustang is believed to have built its XGS-PON FTTP network already

- 0.22 million (7%) are in areas where Project Lightning deployed RFOG FTTP

- 0.16 million (5%) in nexfibre XGS-PON FTTP areas

- 1.77 million (58%) only have a DOCSIS 3.1 coaxial cable network

- 2.52 million (82%) have some form of Virgin Media O2 Gigabit service (various full fibre + coax options)

- 2.13 million* (69%) have Virgin Media O2 Gigabit option over coax but don’t have RFOG or nexfibre available currently; these reflect “new full fibre” connections. Does NOT account for Project Mustang.

* In terms of ‘new full fibre gains’, it is between 1.77m (including Project Mustang) and 2.13m (excluding Project Mustang premises), with the variation dependent on how you treat the Project Mustang XGS-PON footprint, and how far built it is. We have seen various indications of build, but without consumer availability, it can be hard to confirm this.

It is possible the PIA-built Netomnia network (i.e. using Openreach ducting) may be more advanced than the Project Mustang footprint (more on that later when we do an explainer on the types of VMO2 network). This may affect how those premises are provisioned when orders come in.

The total Virgin Media O2 network breaks down as follows (in terms of premises), both currently and a post-acquisition projection based on the current state of rollout (i.e. if it had completed today): –

| Footprint (numbers are premises) | Current VMO2 | Post-Netomnia Acquisition VMO2** | Change |

|---|---|---|---|

| VMO2 Gigabit (all full fibre + co-ax) | 18.81 million | 19.36 million | (+ 0.55 million) |

| VMO2 Project Lightning RFOG footprint | 1.69 million | 1.47 million #assumption | (- 0.22 million) |

| VMO2 nexfibre XGS-PON footprint | 2.13 million | 4.49 million | (+ 2.36 million) |

| VMO2 Project Mustang XGS-PON footprint*** | 3.56 million | 3.18 million #assumption | (- 0.38 million) |

| VMO2 Total Full Fibre footprint*** | 7.16 million | 9.48 million | (+2.32 million) |

| VMO2 DOCSIS-only (no full fibre) footprint | 11.65 million | 9.88 million | (- 1.77 million) |

** These are based on our current tracked figures for each provider from thinkbroadband data.

*** Project Mustang numbers have been hard to track down historically, so this number is higher than previously mentioned.

# For these figures, we are assuming that VMO2 Project Lightning and Project Mustang customers may be moved to Netomnia’s network at the next upgrade point, as they may provide easier scaling. We have seen Project Mustang only be available to new customers for a long time, so we expect some scaling issue exists with existing customers not being moved over yet, hence suspicion they may be more likely to go onto Netomnia’s network. With Project Lightning, the fibre already goes to the property before being converted into legacy DOCSIS, so this may not be as likely due to more cabling work involved, but for Project Mustang, it would depend on the level of infrastructure in place under the street, which is uncertain. These reductions are for illustrative purposes on the assumption that the overlap moves to Netomnia’s network.

Virgin Media O2 / Nexfibre Network Breakdown

Although we need to be clear about the difference between Nexfibre (new build full fibre infrastructure) and VMO2 (retail arm, also with its own legacy network, which includes coax as well as some full fibre), both are owned by the same consortium of companies (VMO2: Liberty Global and Telefonica; Nexfibre: InfraVia, Liberty Global and Telefonica), and therefore, strategies will align. The long-term plan for Nexfibre may well diverge, but so far, these two companies have been very aligned.

There’s a lot of confusion around the terminology used by VMO2 (including in our analysis above), which needs to be broken down for anyone who may not be familiar with this.

- VMO2 DOCSIS — The traditional “cable” broadband network; currently using DOCSIS 3.1 coax (or sometimes referred to as Hybrid Fibre Co-Ax or HFC) that was upgraded from DOCSIS 3.0 standard at the start of this decade. The physical infrastructure was built in the 1990s and 2000s.

- VMO2 Project Lighting (RFOG) — After several years of static footprint, VMO2 embarked on an expansion programme. There was a mixture of extending the existing coax network, but a lot of RFOG (Radio-frequency over glass) full fibre was built mainly from 2016 to 2020. In the past few years, we’ve only seen small additions to that. RFOG uses fibre right up to the outside wall of a home, and then a small media converter is installed that is reverse powered over a short run of coax. The coax enters the home, and the same set-top boxes and modems as used on the older DOCSIS network are then used. This is ‘full fibre’ as the fibre optic connection comes right up to the house. It’s merely converted to old technology there for legacy equipment, but can be switched later.

- Nexfibre XGS-PON — A greenfield build modern full fibre network deployment with fibre taken inside each home as customers order the service. XGS-PON means offering 2Gbps symmetric services for now, but it can deliver 10Gbps if required. IPTV set-top boxes are required, and digital voice. Although they have talked about a wholesale network for other networks to use, we have not seen any non-group company offering it.

- VMO2 Project Mustang XGS-PON — XGS-PON fibre is being rolled out in the street, but to date, the numbers of homes actually having coax removed and the fibre installed is unknown. Households in Project Mustang areas that have never had coax installed will get a ‘full fibre’ install. As of early 2026, it is thought that some limited places in the Project Mustang footprint may be getting coax removed and full fibre installed, but there is no obvious evidence of this happening at any scale yet. The unknowns around premises actually getting full fibre installed mean we don’t yet include Project Mustang as full fibre in our overall full fibre statistics due to its limited availability. We equally don’t list “premises passed” by Altnets when they aren’t able to connect immediately.

We have pulled together these figures from our broadband availability data, which tracks the rollouts. (This has been done rather quickly, so errors may exist.)

Key Conclusions

Nexfibre/VMO2’s shareholders are spending £2 billion to increase VMO2’s Gigabit footprint from 18.81 to 19.36 million premises, an increase of just 0.55 million. The upside is future product potential. VMO2 has been known to push speed boundaries before when competing with Openreach, so we may see a push towards faster services at the retail level, possibly symmetric services to put pressure on Openreach and its key customers like BT.

The VMO2 full fibre footprint increases from 7.16 to 9.88 million premises, an increase of 2.32 million premises, many of which are in areas with existing VMO2 ducting in pavements. These new premises from Netomnia are built primarily on Openreach PIA (physical infrastructure access) products, which means ongoing rental payments due to Openreach. The total conversion of the VMO2 coax footprint to full fibre was meant to be completed by 2028, and yet 9.88 million premises are left even after this acquisition completes.

The second largest Altnet to emerge from the full fibre gold rush is now part of the old guard, which has been challenging the incumbent for a quarter of a century. The sale is a successful exit for Netomnia/Brsk investors, perhaps stronger than a CityFibre acquisition could have been. The question is whether this is going to be good news for consumers, and that depends on what importance you place on a competitive marketplace, given Nexfibre’s lack of wholesale offering.

For the net new fibre in the ground and overbuild, the price tag seems very high. On a pure infrastructure basis, £2 billion to acquire 2.32 million new full fibre premises, many in areas with existing Gigabit network, means a per-premise cost of around £862 (ignoring any value from overbuild of existing infrastructure, which we think might have some value. If you include the full premises without considering overlap, this drops to around £650 (on our numbers), which still isn’t cheap. Of course, VMO2 gets 500,000 customers from YouFibre/Brsk, but it begs the question of how many will stick around (we have already seen comments from users indicating they’ll be leaving YouFibre at the end of their contract due to the acquisition). We suspect the bulk of regular consumers will stay as long as commercials are reasonable; if they can be upsold on television services, it may help to pay some of that acquisition cost.

It will be some time until this deal can be concluded, based on the approvals that will be required.

Test your broadband speed

Test your broadband speed Follow us on X for the latest broadband news

Follow us on X for the latest broadband news

So in simple terms VMO2 are paying out

~£300 per connected customer, plus ~£300 per prems passed

but also taking on existing debt of ~£1800 per customer just to gain additional coverage of 0.55M prems plus

not having to FibreUP 1.8M prems (but with ongoing payments to Openreach) but having to FibreUP / Openreach PIA (Netomnia) 2.1M additional different prems.

The movement of debt has to be financial engineering with overall shareholders to make it worthwhile.