Enders Analysis have warned quite starkly about the unsustainable losses incurred by alternative network operators challenging incumbent Openreach and others on full fibre rollout. In their report titled “UK Altnets: Something’s got to give” they highlight some of the key challenges faced by altnets in the wider competitive landscape.

“Altnet losses expanded to £1.5bn in 2024, as EBITDA losses persisted and interest costs rose sharply, with ARPUs weakening and operating costs stubbornly high, and the increasing interest burden looking unpayable under any reasonable scenario.

Even the best performing altnets can barely make EBITDA breakeven, and not make sufficient margins to cover ongoing customer acquisition investment, resulting in a perpetual cash drain for their investors.

The impact on the rest of the sector is worsening in the short term as pricing falls, but this should accelerate the inevitable consolidation into a sustainable wholesale model under CityFibre and/or VMO2/nexfibre.”

UK Altnets: Something’s got to give, Enders Analysis — Summary

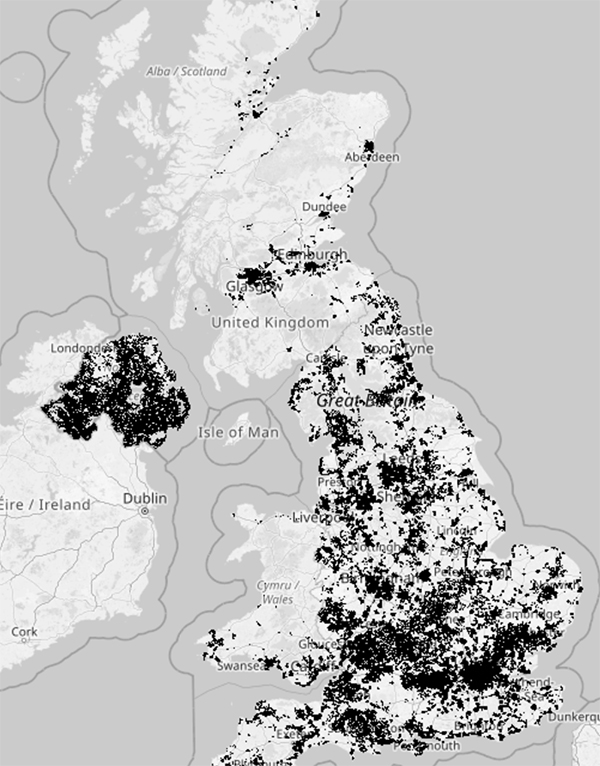

In the past couple of years, most altnets have stopped building and started focussing on take-up, a familiar conversation at many of the altnet events out there such as Connected Britain. The Times wrote last night noting that average penetration rate (i.e. take-up) remains at 15% and the level required for ‘sustainable profitability’ being 40%. This figure is almost impossible to achieve in areas with multiple operators. We noted in our September 2025 Broadband Report that 27% of premises has access to two or more full fibre networks, not taking into account the Gigabit-capable Virgin Media DOCSIS network which remains a valid competitor in consumer’s eyes for the next year or two (and is being overbuilt by Virgin Media fibre network soon too). Obviously there are areas outside of this footprint, but as we reach into 80%+ coverage, the race is getting more and more costly from a ‘per premises’ cost perspective, especially with Openreach’s bold aim to go everywhere.

The problem for many altnets is the lack of a great exit strategy for investors as the market is not willing to pay the price to produce a return for the spend in running fibre to all those premises. We have seem deals like the Brsk/Netomnia merger which has allowed investors to retain their stakes whilst continuing efficiency gains from economies of scale, something which has been speculated on in regards to a potential acquisition of the group CityFibre. We also did a deep dive on the economics of the Virgin Media vs CityFibre options for Netomnia which illustrates the strategic difficulty with overbuild.

With the increasing interest rates affecting all our mortgage costs, the same issue has caused debt repayments for capital intensive infrastructure builders to skyrocket in many cases, putting additional pressure on the businesses. What may have been sustainable in the low interest rate era, simply no longer is.

Those of us who have been around since pre-Internet will remember the sprawl of cable companies in the UK including NTL, Nynex, Telewest and so on who cables up the UK’s busiest streets competing against Sky’s satellite TV offering. This network became the cable competitor for BT’s DSL based services and then converged under Virgin Media. What is happening to altnets is likely to follow a similar path with many in the industry believing considerable consolidation expected in the coming years, with CityFibre potentially leading an independent altnet bid. Although Virgin Media/Nexfibre could potentially try to capitalise on the opportunity to compete against BT, Nexfibre’s rollout is already doing that, meaning that the value which could be added by acquisition may not match the return expectations of altnets.

Many altnets are now offering wholesale access (and aggregators exist to make it easier to do this across networks, although with consolidation this may become less of an issue) to try to increase utilisation across their network, bringing on board companies like Zen Internet and others to retail their services.

Altnets continue to offer some great deals for consumers to sign up, however many plans may not be sustainable. Then again, we all know “brand new customers only” deals with how many large retail operators offer services to try to tempt users away from competitors. Altnets do have one quite significant benefit in that many operate symmetric services, something many heavier users appreciate. They often don’t have traditional commercial business leased line revenue to protect, which means they can offer everyone a great symmetric service.

There is no question in our minds altnets have accelerated the rollout of full fibre across the UK (you can see their impact on our broadband map) and rolled out the fastest connectivity into the most remote of locations. The competition they have brought into the market has been very much in the consumer interest. We expect more consolidation in the altnet space, which may better enable them to get the returns for investors, although new funding will be much harder to get these days than it was some years ago.

Test your broadband speed

Test your broadband speed Follow us on X for the latest broadband news

Follow us on X for the latest broadband news

Enders are recognising what others have been saying since last year.

I was around in the 70/80s working for Visionhire and Rediffusion. They had cable tv networks. 4 channels whoopee. Freeview and Sky killed them off. Prestel was born. I said at the time eventually everybody will be connected and doing their shopping etc online. Wish I’d put a bet on! Sorry but I see the future the same for the internet. Sometime in the future fibre will die to wireless internet. Smart TVs etc will be like giant phones getting their internet via 10g. No one will remeber dialup etc.😂😂Don’t invest in cable.

So why do so many parts of London, like leafy West Norwood in darkest Lambeth still have NO full fibre offering for most of their homes and businesses.

I’m in one such area. The answer depends but the limited fund they have are mostly in place for the absolute best revenue generation. If they don’t have an expectation of significant return they won’t build it with current cost of capital vs revenue opportunity.

I’ve got three sets of fibre going past my rural property – perhaps one of them was supposed to be for you 😀

But seriously – it’s madness. The various companies have probably now laid enough fibre to cover the entire country but because of duplication properties like you have still not been passed.

Same here. In 1 year went from just FTTC to 3 full fibre suppliers.

Mainly because it was government policy to direct investment to the regions with the intent to boost economic activity through high-speed connectivity. Both London and the South East Regions have been held back by this policy, with London left to be the last to be “completed”.

P.S.

Openreach has become more visible and active in South West London in recent months.

The losses are only unsustainable if the companies and their backers decide that they are. They all went into this with their eyes open, knowing that there would be years of loss-making while networks were built and customers signed up. Ofcom and the ASA have done their level best to make the altnets’ job harder by making decisions that favour the incumbent rather than to support and promote a level playing field and give the insurgents a fair chance. The market now is full of consumers that don’t know the difference between full fibre and everything else, and where many of whom are still locked in to high cost low quality low performance contracts with BT. Consolidation in the altnet sector was always inevitable; the surprise is that it hasn’t happened sooner, which suggests that many investors are not yet fretting about their exit strategy, preferring to hold their nerve.

The advertising for part fibre was a major mistake by the regulators early on for sure but for altnets competition/overbuild means they get a smaller share of the market which is the main issue. I think some of the assumptions made may have been wrong.

There has been no favourable treatment for the major players. On the contrary, in the UK, BT/Openreach is now excessively regulated, given the state of the sector. Much of the problem is that regulators will create more bureaucracy so as to be seen to be doing something, while they are reluctant to repeal regulations that are no longer applicable.

The economics have changed against many of the AltNets since many of them first entered the sector. Further, the AltNets had no control over how many players entered the market. The regulator also failed to ensure that only businesses with viable business models could enter the market.

Owners have in recent years shifted focus to try and boost take-up, but this has not been successful for a number of reasons. Now, following the global financial and economic turmoil of the last two years or so, owners have little choice but to work on their exit plans.

I once spoke to an altnet planner who said their job was to spend the investors money.

Could not be more true.

Hardly a surprise. One difference between FTTP and Old-style cable is that at least with cable the physical networks were separate (or so I believe). We’re now in a situation where some properties have multiple physical cables passing them owned by separate companies. What a waste of time and money.

It is called competition.